$0+

What should a beginner invest in?

Investments for Beginners

There are plenty of investment options for beginner investors, including mutual funds and robo-advisors.

The biggest misconception about investing is that it’s reserved for the rich.

That might’ve been true to some extent 10 years ago. But that barrier to entry is gone today, knocked down by companies and services that have made it their mission to make investment options available for everyone, including beginners and those who have just small amounts of money to put to work.

In fact, with so many investments now available to beginners, there’s no excuse to skip out. And that’s good news, because investing is the best way to grow your wealth.

6 ideal investments for beginners

Here are six investments that are well-suited for beginner investors.

1. A 401(k) or other employer retirement plan

If you have a 401(k) or another retirement plan at work, it’s very likely the first place you should put your money — especially if your company matches a portion of your contributions. That match is free money and a guaranteed return on your investment.

You can contribute up to $19,000 to a 401(k) in 2019 (or $25,000 if you’re 50 or older), but that doesn’t mean you have to contribute that much. The beauty of a 401(k) is that there typically isn’t an investment minimum.

That means you can start with as little as 1% of each paycheck, though it’s a good idea to aim for contributing at least as much as your employer match. For example, a common matching arrangement is 50% of the first 6% of your salary you contribute. To capture the full match in that scenario, you would have to contribute 6% of your salary each year. But you can work your way up to that over time.

When you elect to contribute to a 401(k), the money will go directly from your paycheck into the account without ever making it to your bank. Most 401(k) contributions are made pretax. Some 401(k)s today will place your funds by default in a target-date fund — more on those below — but you may have other choices. Here’s how to invest in your 401(k).

To sign up for your 401(k) or learn more about your specific plan, contact your HR department.

2. A robo-advisor

Maybe you’re on this page to eat your peas, so to speak: You know you’re supposed to invest, you’ve managed to scrape together a little bit of money to do so, but you would really rather wash your hands of the whole situation.

There’s good news: You largely can, thanks to robo-advisors. These services manage your investments for you using computer algorithms. Due to low overhead, they charge low fees relative to human investment managers — a robo-advisor typically costs 0.25% to 0.50% of your account balance per year, and many allow you to open an account with no minimum.

They’re a great way for beginners to get started investing because they often require very little money and they do most of the work for you. That’s not to say you shouldn’t keep eyes on your account — this is your money; you never want to be completely hands-off — but a robo-advisor will do the heavy lifting.

And if you’re interested in learning how to invest, but you need a little help getting up to speed, robo-advisors can help there, too. It’s useful to see how the service constructs a portfolio and what investments are used. Some services also offer educational content and tools, and a few even allow you to customize your portfolio to a degree if you wish to experiment a bit in the future.

Here’s more on robo-advisors, along with some of our top picks.

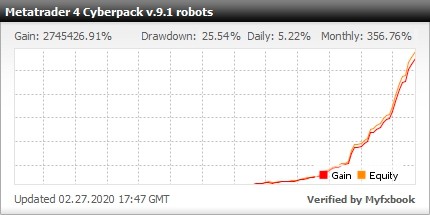

Need more high profit gain and safe robots, here it is Portfolio of expert advisors for trading at Forex market with Metatrader 4 (14 currency pairs, 28 forex robots)

https://forexfactory1.com/p/euhp/

https://www.youtube.com/@forexrobotsforexfactory1si836

3. Target-date mutual funds

These are kind of like the robo-advisor of yore, though they’re still widely used and incredibly popular, especially in employer retirement plans. Target-date mutual funds are retirement investments that automatically invest with your estimated retirement year in mind.

Let’s back up a little and explain what a mutual fund is: essentially, a basket of investments. Investors buy a share in the fund and in doing so, they invest in all of the fund’s holdings with one transaction.

A professional manager typically chooses how the fund is invested, but there will be some kind of general theme: For example, a U.S. equity mutual fund will invest in U.S. stocks (also called equities).

A target-date mutual fund often holds a mix of stocks and bonds. If you plan to retire in 30 years, you could choose a target-date fund with 2050 in the name. That fund will initially hold mostly stocks since your retirement date is far away, and stock returns tend to be higher over the long term.

Over time, it will slowly shift some of your money toward bonds, following the general guideline that you want to take a bit less risk as you approach retirement.

4. Index funds

Index funds are like mutual funds on autopilot: Rather than employing a professional manager to build and maintain the fund’s portfolio of investments, index funds track a market index.

A market index is a selection of investments that represent a portion of the market. For example, the S&P 500 is a market index that holds the stocks of roughly 500 of the largest companies in the U.S. An S&P 500 index fund would aim to mirror the performance of the S&P 500, buying the stocks in that index.

Because index funds take a passive approach to investing by tracking a market index rather than using professional portfolio management, they tend to carry lower expense ratios — a fee charged based on the amount you have invested — than mutual funds. But like mutual funds, investors in index funds are buying a chunk of the market in one transaction.

Index funds can have minimum investment requirements, but some brokerage firms, including Fidelity and Charles Schwab, offer a selection of index funds with no minimum. That means you can begin investing in an index fund for less than $100.

5. Exchange-traded funds

ETFs operate in many of the same ways as index funds: They typically track a market index and take a passive approach to investing. They also tend to have lower fees than mutual funds. Just like an index fund, you can buy an ETF that tracks a market index like the S&P 500.

The main difference between ETFs and index funds is that rather than carrying a minimum investment, ETFs are traded throughout the day and investors buy them for a share price, which like a stock price, can fluctuate. That share price is essentially the ETF’s investment minimum, and depending on the fund, it can range from under $100 to $300 or more.

Because ETFs are traded like a stock, brokers often charge a commission to buy or sell them. But many brokers, including the ones on this list of the best ETF brokers, have a selection of commission-free ETFs. If you plan to regularly invest in an ETF — as many investors do, by making automatic investments each month or week — you should choose a commission-free ETF so you aren’t paying a commission each time. (Here’s some background about commissions and other investment fees.)

6. Investment apps

Several investing apps target beginner investors.

One is Acorns, which rounds up your purchases on linked debit or credit cards and invests the change in a diversified portfolio of ETFs. On that end, it works like a robo-advisor, managing that portfolio for you. There is no minimum to open an Acorns account, and the service will start investing for you once you’ve accumulated at least $5 in round-ups. You can also make lump-sum deposits.

Acorns charges $1 a month for a standard investment account and $2 a month for an individual retirement account. Our unsolicited advice: Max out that IRA account before you start using the standard investment account — there are tax perks to the IRA that you don’t want to miss. (Learn more about IRAs here.)

Another app option is Stash, which helps teach beginner investors how to build their own portfolios out of ETFs and individual stocks. Stash carries just a $5 account minimum and has a similar fee structure to Acorns, though balances that top $5,000 are charged 0.25% of that balance per year, rather than the flat fee.

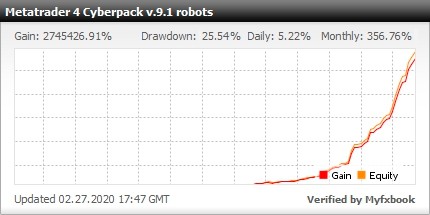

Need more high profit gain and safe robots, here it is Portfolio of expert advisors for trading at Forex market with Metatrader 4 (14 currency pairs, 28 forex robots)

https://forexfactory1.com/p/euhp/

https://www.youtube.com/@forexrobotsforexfactory1si836