$5+

Yen near seven-month high versus dollar; Hong Kong, Argentina woes fuel risk aversion

The yen traded close to a seven-month high against the dollar on Tuesday, as unrest in Hong Kong and gyrations in Argentina's markets heightened investor risk aversion and fanned demand for the safe-haven Japanese currency.

The yen was at 105.495 per dollar after brushing 105.050 overnight, its strongest since Jan. 3.

The Japanese currency, which attracts flight-to-safety flows in times of market turmoil, has been on a solid footing this month, supported by factors such as U.S.-China trade tensions and the prospect of further monetary easing by the U.S. Federal Reserve.

The currency has received a fresh boost from deepening unrest in Hong Kong, where the international airport was closed to flights for several hours on Monday amid ongoing demonstrations. Surprise primary election results in Argentina, which resulted in a rout in the country's peso currency, stocks and bonds, have also added support.

"It's the 'risk off' in the market generated by events in Hong Kong and Argentina that is feeding demand for the yen," said Yukio Ishizuki, senior currency strategist at Daiwa Securities. "Speculators are increasing their long positions on the yen."

"There really are no signs of the yen's advance abating," Ishizuki added. "The next target is the yen's high reached against the dollar early in January, but even that threshold won't present much of an obstacle at this rate."

The Japanese currency has gained for the past four trading days against the greenback. A move beyond 104.100 per dollar, this year's high scaled at the start of January, would take the yen to its highest level since November 2016.

"The shrinking spread between U.S. and Japanese yields has thrust dollar/yen into a downtrend, despite recent bouts of global equity market strength," said Junichi Ishikawa, senior FX strategist at IG Securities in Tokyo.

U.S. Treasury yields have declined steadily on the back of global economic concerns and the prospect of the Fed cutting rates in the months ahead. The spread between U.S. and Japanese benchmark 10-year yields has shrunk to its narrowest since November 2016 this month as a result.

The euro (EUR=) dipped 0.25% to $1.1188, handing back the previous day's modest gains.

The single currency had edged higher on Monday after Italian bond yields pulled back from five-week highs on relief that rating agency Fitch left the country's credit rating unchanged.

Longer-term prospects for the euro remain grim with the European Central Bank widely expected to ease policy as early as September and on lingering concerns towards Italy, where its deputy prime minister and right-wing League party leader Matteo Salvini has called for early elections.

The Australian dollar crawled up 0.15% to $0.6759 as the Chinese yuan found a bit of traction after the People's Bank of China set a midpoint rate at a fresh 11-year low but a level that was firmer than expected.

The Aussie had lost 0.5% the previous day, slipping in sympathy with the yuan amid little sign of progress in U.S.-China trade relations. The Aussie is sensitive to developments in China, Australia's largest trading partner.

Argentina's peso lost roughly 15% to 52.15 per dollar on Monday after brushing an all-time low of 61.99.

Fears of a possible return to interventionist policies, and by extension a possible debt default, gripped the market after conservative Argentina President Mauricio Macri lost by a much wider-than-expected margin to the opposition in presidential primaries.

====================================================================

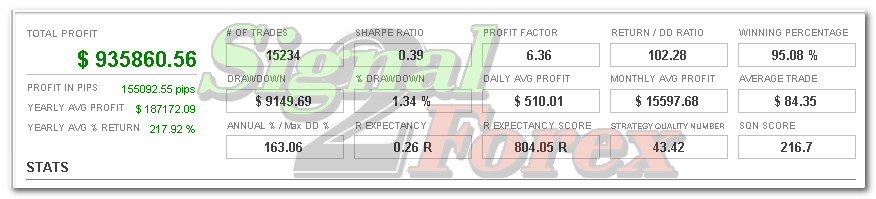

BEST FOREX ROBOT - Portfolio of expert advisors for trading at Forex market with Metatrader 4 (14 currency pairs, 28 forex robots)

YOUTUBE REAL TIME VIDEO TRADING

====================================================================